Commentary

There is the reality all around us—restaurants struggling to survive, bills eating household income, jobs ever less secure, costs soaring for all enterprise, even the local dollar stores hitting hard times—and there are the macroeconomic statistics reported daily by the media. They seem to have ever less connection to each other.

Why do we have macroeconomic statistics? We all want to know more about the world outside of our direct experience. That is especially true for those whose livelihoods are bound up with knowing. For economics, that includes academics, investors, and just regular business people who are trying to make plans and would like to make sense of their prospects in a different market.

Starting about a century ago, a new market for data opened up. It was for government planners to exercise newly granted powers to plan the economy better than markets. The idea was that with better data, they could do a better job in adjusting outcomes in a way that would be more socially optimal.

The data collection industry was born. And it grew and grew, taking a huge leap in the 1930s during which time governments and central banks embarked upon a grand plan to tame business and trade cycles. They imagined themselves to have various levers in control rooms, with handles and names like “fiscal policy” and “monetary policy.” They would pull and push these levers to smooth out the recklessness of markets.

If you head to Washington, D.C. today and go to the Federal Trade Commision, you will see an impressive statue from the 1930s called “Man Controlling Trade.” It’s a muscular man representing government and a wild horse representing the market economy. The man is successfully keeping the market in check. That’s how it was imagined to work back then and still today.

Related Stories

To be sure, we’ve learned that the reality is otherwise. It is more like the horse is riding the man or actually the horse is pulling the man, depending on your perspective. The man only intervenes to get something for himself, not serve the public. If that outlook sounds dark, have a look at the operation of any sector of economic life and look at it honestly. You will see, if you look carefully, that the storied vision of how it is supposed to work contradicts the reality.

In any case, back to statistics. Consistent with the way in which our times have lost faith in so much of what is called “science,” the science of data collection for purposes of economic planning has not gone well. For instance, back in the 1960s, it was widely believed that there was a consistent tradeoff between inflation and unemployment. When one was up, the other was down. It was said to be possible to control each element by manipulating the other.

To some extent, the Fed’s Jerome Powell seems to believe something like this now. His idea of controlling inflation was not, at least overtly, to better manage the money stock but rather to “slow down” economic growth that is believed to be the underlying cause of inflation. At least that is what he said.

And yet when you think about this alleged tradeoff, it keeps being contradicted by reality. In the 1970s, we saw our first big bout of what was named stagflation, when both inflation and unemployment were high. At that point, the Fed had no idea what to do. And in our own time, we had low inflation and low unemployment for nearly two decades when suddenly they began to see-saw in strange ways with lockdowns. Unemployment soared but inflation stayed low, until inflation rose and unemployment went back down. Now we are seeing inflation still high and unemployment rising with it.

That’s a problem with the theory, but there’s an even more fundamental problem with the data collection itself. When we see numbers and charts, there is something in the modern human brain that suspends incredulity. We simply take it for granted that what we are seeing is true.

We saw this in COVID. The charts were everywhere: exposure, infection, cases, hospitalizations, and deaths, and they were presented in waves. We thought we were following the science. We were told to look at the data and follow the science. We heard it over and over like a mantra. But people rarely if ever stopped and wondered: is any of this even true?

Obviously the case and infection data is entirely contingent on testing, and the testing results were themselves contingent on accuracy, and the death data were contingent upon a judgment call concerning the cause of death. Put it all together with possible errors and what do you end up with? We came to realize that much of what we were being told was accurate was in fact complete gibberish.

Sadly, the same thing is happening in economics today. What the Bureau of Labor Statistics reports as true inflation does not comport with anything being pushed by industry. Groceries are a good example. The Consumer Price Index (CPI) lists them as up 20 percent over four years but industry puts the figure closer to 34 percent. It’s the same with cars: the rates of inflation are double what government reports. Meanwhile, many costs are not reported at all, such as taxes, interest, or home prices.

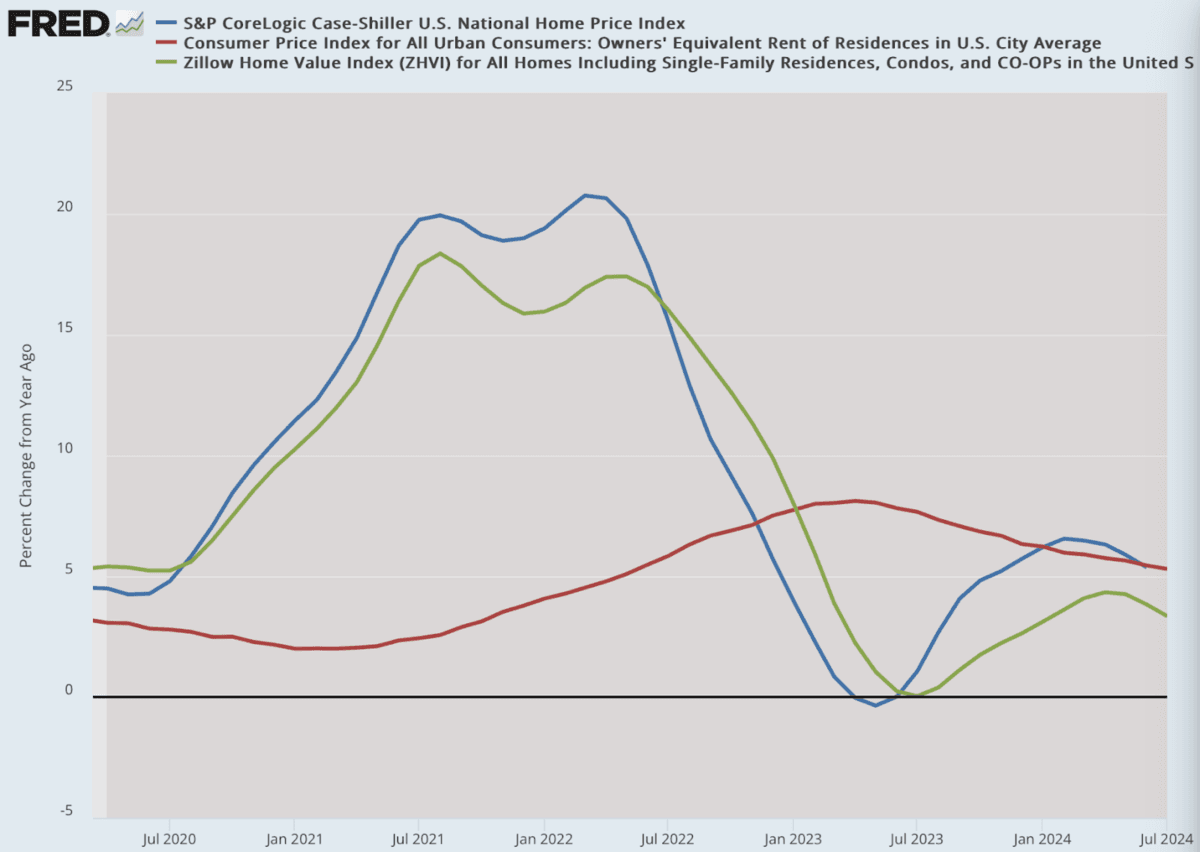

It reaches absurdity with home prices because government reports “Owners Equivalent Rent” rather than, you know, the actual home prices. We end up with figures that are twice as high as government reports.

(Data: Federal Reserve Economic Data (FRED), St.

The Unreliable Nature of Economic Data

It is important to take Gross Domestic Product (GDP) numbers with caution, as a significant portion of the figure is due to increases in government spending. Excluding this, the numbers can turn from positive to negative, especially when adjusted for actual inflation rates. This can reveal recessionary conditions that may not be immediately apparent.

Recent revelations have shown that job numbers have been overstated by around 1.2 million jobs that do not actually exist. This discrepancy can be attributed to a statistical adjustment known as the “birth-death” rate used by the Bureau of Labor Statistics (BLS) to estimate business formation and closure. This method, based on historical data and survey results, often leads to inaccurate representations of the true economic landscape.

Furthermore, the current economic climate, particularly due to lockdown measures, has caused widespread business failures. The BLS model, however, seems to ignore these conditions, leading to potentially misleading job data. It is likely that post-election revisions will reveal a more accurate, albeit grim, economic picture.

Looking ahead, it is anticipated that there will be significant downward revisions and the possibility of a recession extending back to March 2020. The lack of transparency and reliability in government data collection and reporting is a concerning issue that undermines public trust in economic indicators.

As noted by Murray Rothbard, the reliance on government data for economic planning and regulation can have serious consequences when the data itself is not trustworthy. In an age where data drives decision-making processes, the prevalence of inaccurate or manipulated data poses a significant challenge to sound economic analysis.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times.

Image source: Louis Fed; Chart: Jeffrey A. Tucker)Data: Federal Reserve Economic Data (FRED)