Commentary

June’s year-over-year Consumer Price Index is still running 3 percent, which is now considered more-or-less on target. Five years ago, that would have been seen as intolerably high. The month-over-month decline of 0.1 percent, the best in a year, was driven by gas and used cars, which are reported as down 10 percent year over year (but still up 30 percent over four years).

So while the financial press trumpeted the great news for consumers, there needs to be some context here. This is a minor blip, heavily influenced by what it excludes not to mention adjustments we cannot see, and easily reversed.

Some people speculate that 3 percent is the new target and that the old 2 percent standard is being deprecated. That very well might be true. That’s very bad news for consumers and small businesses, however. It means that incomes will continue to have a hard time keeping up with purchasing power.

This perception is reinforced by the Producer Price Index (PPI), which garners far less attention, but which clearly shows signs of re-acceleration. The year-over-year changes are worse than in a full year.

Related Stories

This report prepares the Federal Reserve for what has been the intention since early in the year. It wanted to cut interest rates in the fall. This seems highly likely. The expectation of the rate cut has been a driving force for higher financials and will continue for the duration. Wall Street is booming in ways that fundamentals simply cannot support, and everyone knows that. Loose credit, however, can indeed keep the magic going for a very long time.

Many people who are hoping to buy a house on a 30-year mortgage might welcome a rate cut. But we need to be clear about what the Fed can and cannot do. It can control its overnight lending rates to member banks. It cannot determine how that will affect the full shape of the yield curve.

It’s entirely possible that with a rate cut, the yield curve will simply become steeper, with rates on 5 and 10-year bonds, including 30-year mortgage rates, staying the same or even rising. It also does not directly affect interest in credit card debt, which is already floating between 20 and 23 percent.

The market function of the yield curve is to allocate credit to its most valued ends. All else equal, higher rates should discourage borrowing and encourage savings. In this cycle, however, that is absolutely not happening. As household income has become squeezed, credit card debt has risen dramatically while delinquent payments are starting to rise also.

Meanwhile, the personal savings rate has fallen instead of risen.

How can we account for this? It’s rather simple: responding to interest rate signals requires discretionary income, which people simply do not have following the high levels of spending during lockdowns and the subsequent inflationary ravaging of whatever was remaining. It was one of economic history’s greatest head fakes, during which time people thought they were rich only to find they were suddenly poor again.

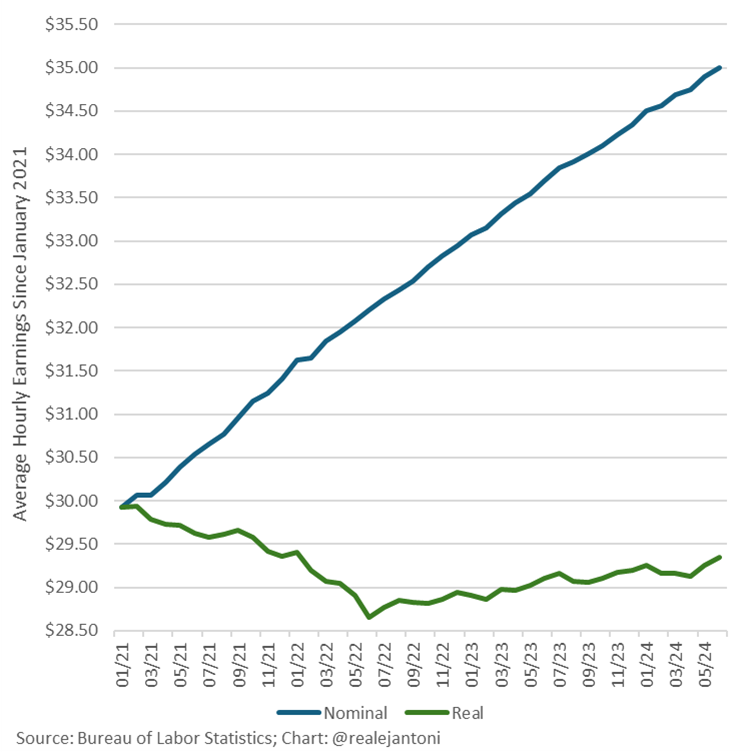

Measuring precisely how much this is true is not easy. The official inflation numbers may not entirely represent the reality of what people have been experiencing. Over five years, the Consumer Price Index (CPI) registers 23 cents in lost purchasing power of the dollar in terms of U.S. goods and services.

You can find products out there that seem to reflect that, mostly those involving consumer electronics and some items of clothing. But overall? It’s hard to believe that this number represents any real-world basket of goods.

Consider fast food, for example. In 2019, a McDonald’s cheeseburger was $1. Now it is $3.15. A Big Mac was $4. Now it is $7.50. Overall, the prices at the most popular chain are up 141.4 percent. That is a far cry from 23 percent. So too for Chick-fil-A. The signature sandwich was $3.65 but is now $6.55. Overall, prices at this restaurant are up 80 percent. At Burger King, prices are up 85.7 percent, at Taco Bell they are up 57.4 percent, and at In-N-Out Burger, prices are up 55 percent.

Let’s talk about housing, which is up 41–49 percent over the same period. This is not included in the CPI, which also does not include interest-rate increases, which are up by 100 percent over this period. The Fed does track both, however, even if the CPI excludes it.

The Truth About Inflation and the Economy

Inflation has been a hot topic lately, with conflicting reports from various sources. The Bureau of Labor Statistics (BLS) claims that inflation is under control, but industry data tells a different story. According to the St. Louis Fed, the Consumer Price Index (CPI) has been rising steadily, contradicting the BLS’s narrative.

Additionally, health insurance premiums are on the rise, despite what the BLS reports. According to KFF, premiums have increased by 20 percent since 2021, contradicting the BLS’s claim of a 19 percent decrease.

When we delve into industry data, we see discrepancies between government reports and reality. Exclusions and adjustments skew the numbers, making it difficult to get an accurate picture of the economy.

Both the government and industry have reasons to downplay inflation, leading to a lack of transparency in economic data. With no solid basis for a rate cut in the near future, the risks of such a move could have long-term consequences.

In the past, rate cuts meant to combat inflation have backfired, leading to hyperinflation. The current economic climate, coupled with excessive government spending, creates a precarious situation that could worsen with misguided policies.

Despite concerns of an impending economic crisis, the real threat lies in stagnant growth and persistent inflation. Another rate cut could reignite inflation, leading to a prolonged period of economic decline.

It’s essential to critically analyze economic data and policy decisions to prevent a potential crisis. The future of the economy hinges on informed and strategic actions to address the underlying issues.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times.

Please rewrite this sentence.

Source link