Commentary

The announcement that national output grew faster than expected in the second quarter should have generated some relief and optimism. Oddly, it did not. The news was greeted by Wall Street and Main Street as no big deal. In fact, the broader stock market indexes were down, including S&P and Nasdaq, before recovering some losses.

Why might this be true? Normal intuition might suggest that a glowing gross domestic product (GDP) report would infuse the financial markets with optimism about economic growth and that this would be a big buy signal. This does not seem to have happened.

Part of the reason is that the data now coming out from the federal government has become highly suspect. The jobs data, the inflation data, and even the GDP data has become a tool for political propaganda. Indeed, this was how it was immediately deployed. This is a rather new trend but it is well known.

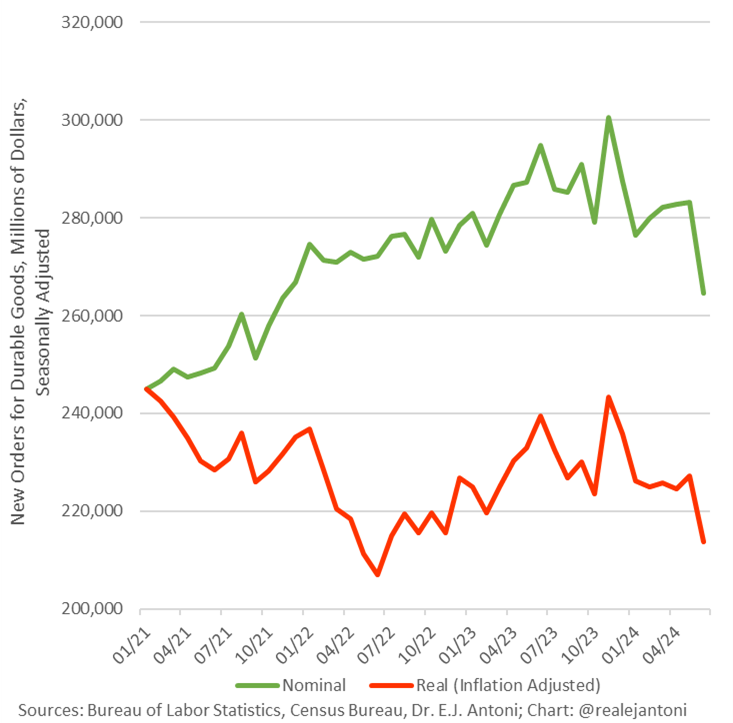

In this case, the GDP data is reported in “real” terms meaning adjusted for inflation. But the inflation adjustment used in this case is not the consumer price index (CPI), which rose 2.8 percent over the period (which is wildly underestimated). Instead, the GDP uses a statistical category called Personal Consumption Expenditures (PCE), and during that period estimates inflation at a much lower level of 2.3 percent. Replacing one with the other zeroes out the gain.

In other words, this is a minor statistical issue having to do with how we calculate inflation. Neither the CPI nor the PCE state the real rate of inflation because they both exclude real home prices, interest rates, an accurate and plain reading of health insurance or home insurance, and do not account for added fees or shrinkflation, which is a major way in which inflation has expressed itself. The PCE is the best-possible source from the government’s point of view.

Related Stories

If the data were adjusted by an actual accurate number, the growth would vanish. That’s not only true in this reporting period but every reporting period for three years now. The understatement of inflation has a devastating and distorting effect on this data. Everyone with skin in the game knows this.

In other words, it makes no sense to count dollars and cents changing hands as economic growth if those dollars and cents are losing value dramatically, perhaps 20 percent but as much as 50 percent or more, depending on the sector, over the last four years.

How might the data be revised in light of this reality? Economists are working on this very issue right now.

Added to that we have the major problem that government spending has hit wartime-level increases over four years, exceeding that of the second world war. All of this spending is counted as economic growth and has been since the 1930s. In normal times, provided government spending increases at a stable level, this is not a problem. But when there is a sharp and sudden change in the trend line, the data becomes seriously distorted.

Federal debt as a percentage of Gross National Product has hit new records. This discredits all the GDP reports coming out right now. This is not an unknown fact. It remains as high today as it was in 1946.

Economists have known for many decades that data from wartime is unreliable. The notion that World War II granted U.S. prosperity is so preposterous as to refute itself. The nation sacrificed enormously during that period. Patriotism was high but prosperity was not. Rationing tickets governed the shopping experience. Deprivation was everywhere in sight. Men had been drafted into war and were missing from communities.

This is the nature of wartime. Call it what you want but economic growth is not the first thing that comes to mind. Indeed, the Great Depression did not truly end until the war’s end. What, then, can be said about this strange period in which debt-to-GDP reached wartime levels? How much has that distorted our data?

There is another problem with the data. It is not as stable and integrated over time as it once was. This is because the lockdowns of 2020 blew up all the normal metrics, from jobs numbers to output following a reasonably predictable pattern. But with lockdowns, everything about this undertaking went haywire, including even the ability to collect the data itself.

As a result, the data is no longer considered credible, essentially by anyone. The lead offenders here are the reporting on jobs and price increases. The errors are so extreme at this point that the reporting itself is largely disregarded as not serious. And this widespread incredulity has affected GDP data too, to the point that the latest releases have been reduced to statistical noise.

There is another consideration too. Even if the releases are not considered serious or true, everyone is aware that the policies of the Federal Reserve are still affected by them.

The financial markets are heavily influenced by the perceived actions of the Federal Reserve. Currently, the stock market bubble is seeking more credit, putting pressure on the Fed to lower rates. This results in a paradox where bad news is seen as good news because it may lead to more monetary stimulus, while good news is viewed as bad news as it reduces the case for rate cuts. This market psychology reflects a sense of unreality and skepticism towards data releases, which are often seen as fake news. Despite signs of economic activity, there is a general disbelief in the accuracy of official data sets. It is important to trust your own observations and remain skeptical of external descriptions of reality.

Source link